Teleworking abroad after Corona – What is the impact on the labour cost?

After the Corona crisis, teleworking is on everyone’s minds. Your employee wants to continue working from home, but what if “home” is just across the border in a neighbouring country? As an employer, you face certain risks if you do not take the necessary measures in time.

The temporary tolerances due to Covid expire on 30 June 2022. This may result in the employer having to pay social security contributions and wage withholding taxes in the employee’s country of residence rather than in the employer’s country of establishment.

Permission of the employer

Telework at the employee’s place of residence or at another location chosen by the employee is possible by mutual agreement between the employee and the employer. Thus, in a first step, the employer must either give the employee permission to telework or not. A written agreement, or at least detailed instructions, are a must to clarify what the exact telework place is, for how many days per week/month this applies, etc.

Before making a decision, you should therefore consider the impact on your business.

In which country does the employer have to pay social security contributions?

Telework has implications for the social security position of workers employed across borders.

The physical presence of the worker in the territory of a given country during the performance of his work is one of the decisive elements for determining the applicable social security scheme. Increasing teleworking abroad may therefore lead to a change in this situation. EC Regulation 883/2004 stipulates that a worker is covered by social security in the country of employment (“lex loci laboris”). However, if a worker carries out a substantial activity (at least 25% of his working time) in his country of residence, the social security system of his country of residence applies.

Due to the Corona crisis, as from 13 March 202, the Belgian government had decided not to take into account periods of telework on the Belgian territory for the assessment of applicable social security. The same position was taken by a number of other member states, including our neighbours the Netherlands, France, Germany and Luxembourg.

Until 30 June 2022, changes in work patterns that are a direct and exclusive consequence of the Covid pandemic will not lead to a change in the social security system. However, if the work pattern does not “normalise” after this date and the worker continues to telework abroad structurally and substantially, he must take into account the social security system of that home country as of 1 July 2022. The employer must register in advance with the local social security authority in order to correctly carry out the required registrations and declarations.

The impact on the employee’s wage cost is also not insignificant. The financing of social security in other countries differs from the Belgian system. However, it is good that contributions are often lower than in Belgium.

Which country is authorised to levy income tax?

The agreements that the Belgian tax authorities had previously concluded with the tax authorities of our neighbouring countries Luxembourg, France, the Netherlands and Germany had also been extended until 30 June 2022. Until then, the tax authorities consider Corona teleworking days as working days in the country of normal employment. The normal country of employment will therefore continue to tax the income earned by the workers concerned on the days they telework.

However, the agreements contained in the double taxation treaties will once again become fully effective as of 1 July 2022, which means that income tax is generally due in the employee’s country of residence. Employees who are employed in a cross-border context (e.g. working in several countries or making many business trips), on the other hand, will usually be taxable in the country where they physically work. The decisive factor is the actual presence of the employee in the countries concerned. For Belgian residents, this often leads to a tax advantage, as the tax burden in other countries is usually a bit lower than in Belgium.

Tip: Keep a precise record of the days you work abroad.

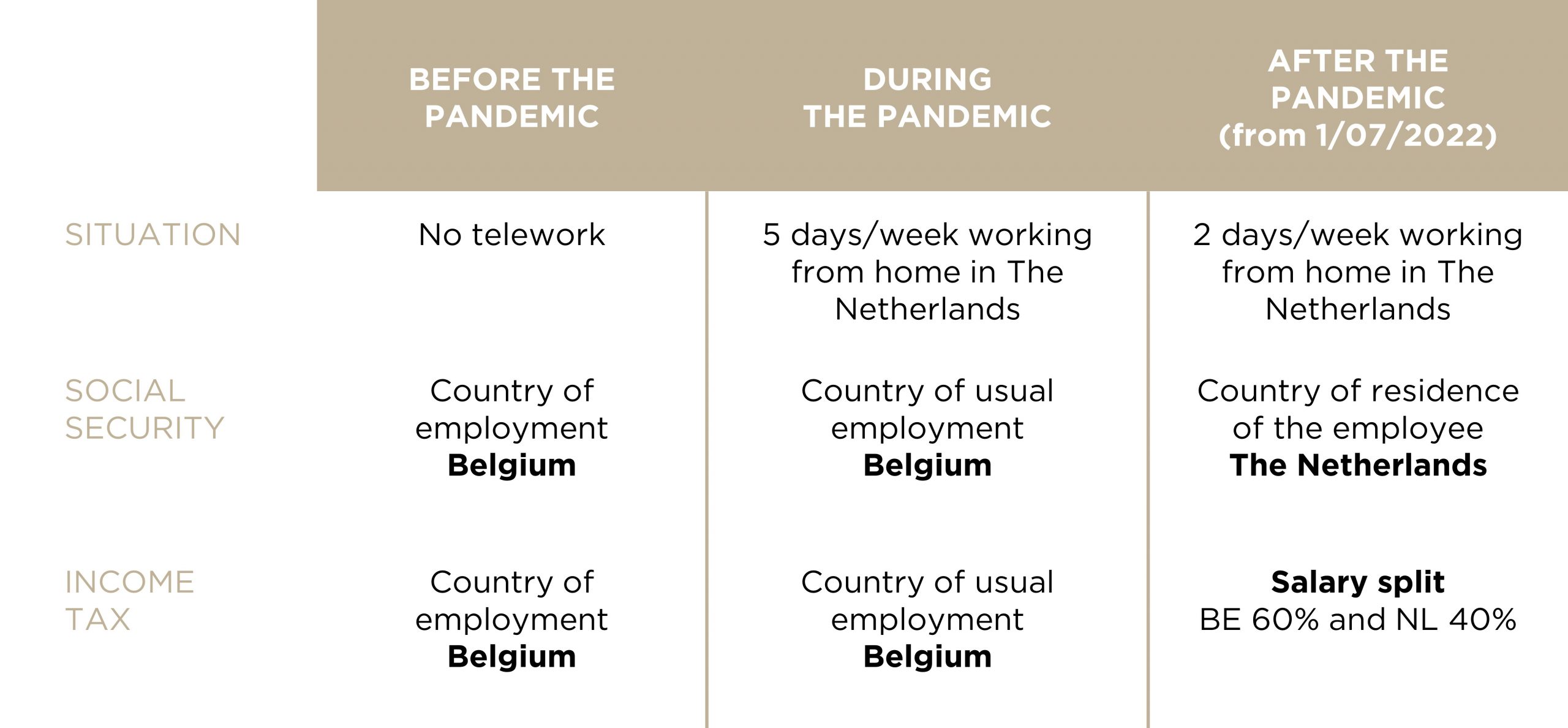

Example: consequences of teleworking post-Corona

Impact on wage cost and net salary – example calculation

Situation: Employer established in Belgium and (single) employee residing in the Netherlands with a gross annual salary of € 50,000.

As our example shows, the use of cross-border (tele)work can be financially beneficial for both employers and employees.

Obligations in the employee’s country of residence

Companies that allow their foreign workers to (continue to) telework must consider a number of additional obligations. Just as for domestic workers, they must consider the necessary arrangements for the home office, the possible rental of a satellite office or the reimbursement of the costs or the implementation of a telework allowance.

In addition, before 30 June 2022, you should evaluate the situation of each teleworking employee so that you can complete the necessary formalities with the local social security authority and tax authority in time.

If you would like more information about cross-border employment and how you can organise yourself accordingly as a company, please contact us.

Publication date: 13/06/2022