NEW TRANSFER PRICING FORMS PUBLISHED AS FROM FINANCIAL YEAR 2016 – HEADS UP ON THE TRANSFER PRICING DOCUMENTATION!

Like many other countries, Belgium has adopted the new transfer pricing documentation requirements from the OECD “BEPS” action plan.

In short, multinational groups being present in Belgium through a company or permanent establishment need to assess whether they are required to file a master file, local file or country-by-country report with the Belgian tax administration.

The new requirements apply as from financial years beginning on 1 January 2016 or later.

Complying with the new transfer pricing documentation requirements needs to be done through specific forms which the Belgian Government has now released. The ultimate filing due date is not the same for all forms, but a large part of the documentation needs to be filed as an annex to the corporate income tax return. As a result, many companies and permanent establishments will need to have their documentation in place ultimately in September 2017 before they can proceed to filing their Belgian income tax return.

In this newsflash we guide you through the main attention points in a general overview.

Master file

All Belgian entities, being both Belgian corporations belonging to a multinational group as well as Belgian permanent establishments of a foreign company, are required to file a master file through a form 275 MF if one (or more) of the thresholds below were exceeded in the previous financial year. Please bear in mind that these thresholds need to be assessed on a stand-alone basis.

- An annual average of full-time employees > 100

- Operational and financial income combined > 50 million EUR

- A balance sheet total > 1 billion EUR

The purpose of the master file is to provide general insight into the multinational group to which the entity or permanent establishment belongs. The form 275 MF needs to be filed within 12 months following the closing date of the financial year concerned. Information which needs to be disclosed is as follows:

Local file

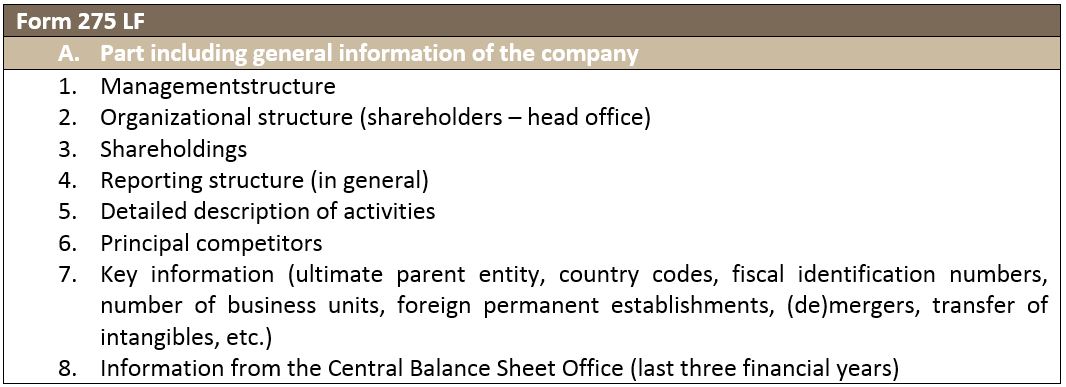

All Belgian entities required to file a master file will automatically also have to file a local file through form 275 LF. On the one hand, the local file form consists of a part in which general company information needs to be reported. Information which needs to be disclosed is as follows:

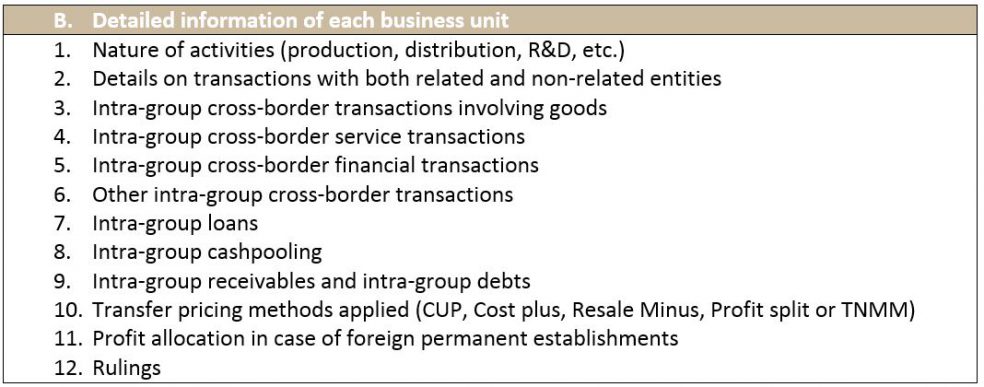

On the other hand, also a part requesting detailed information of business units needs to be completed per business unit which has conducted cross-border transactions with group entities totaling more than 1 million EUR during the previous financial year. Companies will thus have to reflect on how their business is divided into different business units. Such division into business units should be aligned to the current organizational and/or reporting structure. The information to be disclosed is as follows:

As opposed to the master file, form 275 LF needs to be filed together with the income tax return for financial years beginning 1 January 2016 (or later). The part requesting detailed information of business units however only needs to be completed for financial years beginning 1 January 2017 (or later).

Country-by-country report

A third part of the new transfer pricing documentation concerns the country-by-country report, for which form 275 CBC has been introduced. The country-by-country report aims at providing an overview of the group broken down into each country in which the group is active through a legal entity or permanent establishment. Amongst the information elements requested in the overview are main activities, number of employees, income taxes paid or due and other economic indicators.

Filing a country-by-country report is only mandatory for multinational groups having a consolidated turnover of more than 750 million EUR in the preceding financial year. In principle, the Belgian entity of the group only needs to file the country-by-country report if it is the ultimate parent entity of the group. It should be noted however that exceptions might apply under which the Belgian entity or Belgian permanent establishment must file the country-by-country report despite not being the ultimate parent entity. The country-by-country report needs to be filed ultimately 12 months after the closing date of the financial year.

A notification form 275 CBC NOT has been introduced in order for all Belgian entities or permanent establishments of qualifying multinational groups to notify to the Belgian tax administration in advance which group entity will have to file the country-by-country report within the group. This form must be filed no later than the final day of the financial year. An extension of the filing due date until 30 September 2017 has been granted for the first time a notification needs to be done.

Documentation requirements to be checked for each country

Other countries have introduced new transfer pricing documentation requirements as well, but other criteria might apply. For example, should the group be present in the Netherlands, then the € 50 million threshold should be assessed on a consolidated basis (while in Belgium it should be assessed on a stand-alone basis, see above). Hence, a documentation requirement could become applicable in the Netherlands while it would not have become applicable in Belgium. The fact that the group’s presence in the Netherlands might be very limited on its own is not taken into account.

Have you started yet with the preparation of the transfer pricing documentation?

A large part of the documentation needs to be filed as an annex to the corporate income tax return. As a result, many companies and permanent establishments will need to have their documentation in place ultimately in September 2017 before they can proceed to filing their Belgian income tax return. Other countries might have set different filing due dates. Therefore, it is advisable to start with the preparation of the transfer pricing documentation as soon as possible.

Companies not complying with the documentation requirements are facing the risk of in-depth and time-consuming transfer pricing audits, tax increases resulting in international double taxation, a reversed burden of proof with respect to the deductibility of costs and, last but not least, administrative fines up to € 25.000.

In cooperation with our international network we can assist you by mapping out all the transfer pricing documentation requirements applicable within the group and systematically assist with the preparation and filing of the documentation itself.

Transfer pricing strategy can lead to tax optimization

The importance of the right transfer pricing strategy cannot be overestimated. The preparation of the new transfer pricing forms could be an opportunity to (re-)evaluate the current transfer pricing group policy. In practice we have noted that changes made to transfer pricing policies, in order to update them or make them more accurate, have resulted in tax savings on group level.

Another important item for multinational enterprises are intellectual property rights and how to optimize the flow of revenue within the group related thereto (for example sale or licensing of IP). Van Havermaet experts can advise on the many tax incentives Belgium has to offer to innovating businesses. In particular, the new tax deduction for innovation income covering software and patented products or procedures will be of great support to many companies as from 1 July 2016. In this respect, attention should also be paid to contractual arrangements being at arm’s length.

At Van Havermaet, we are eager to provide you with more in-depth information, to assess your situation and to assist you with the preparation and filing of the documentation in cooperation with our partners from our international network Morison KSi.

Publication date: 02 januari 2017