New invoice statement for Belgian contractors applying “VAT reverse charge”

Belgian contractors carrying out works in immovable state may not charge VAT to their contracting partner if the latter submits periodic VAT returns. The “VAT reverse charge” scheme has certain imperfections and will therefore be amended with effect from 1 January 2023. In future, contractors will have to add an additional mention on their invoice.

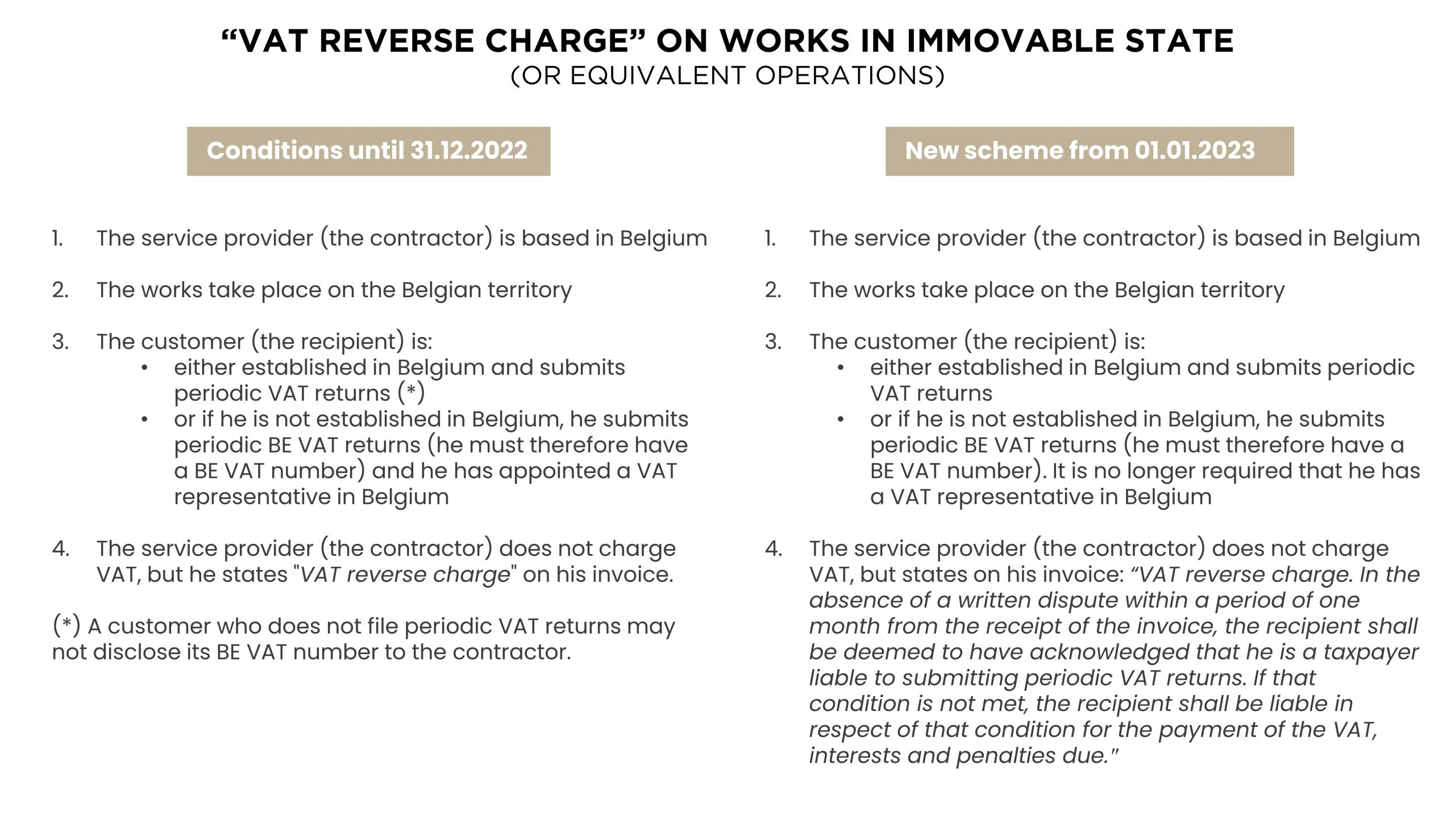

The scheme until 31.12.2022

When Belgian contractors carry out works in immovable state or perform equivalent operations in Belgium, they are not allowed to charge VAT to their contracting partner. Provided certain conditions are met, a reverse charge mechanism allows to designate the recipient of the services as the person liable for the payment of VAT (RD No. 1, art. 20).

If the recipient is a business established in Belgium then it must file periodic VAT returns (monthly or quarterly returns). Businesses who do not submit periodic returns are therefore not eligible for the reverse charge scheme, but this is where the problem lies. Although some taxpayers have a BE VAT number, they do not submit periodic VAT returns. This is the case, among others, for the so-called “small companies” (turnover < EUR 25,000) and “flat-rate farmers”. If – despite a strict ban introduced in 2018 – they still communicate their BE VAT number to the contractor, it is not always clear to the latter whether he may apply the reverse charge rule. A further adjustment was therefore required.

If the recipient is not established in Belgium, then he must file periodic VAT returns (i.e. he must have a BE VAT number), but he must also have a VAT representative in Belgium, which is not easy for a contractor to check. This too is remedied by the new regulation.

The new scheme from 01.01.2023

The ban on “small businesses” and “flat-rate farmers” communicating their BE VAT number will be abolished. From now on, they – like any taxpayer – must communicate their VAT number to the contractor, however they must also inform the contractor that they do not meet the conditions for the application of the reverse charge scheme. It seems quite probable, that this will not happen in practice. In order to still absolve the contractor from liability for not charging VAT, he should in future include the following statement on his invoice:

“VAT reverse charge. In the absence of a written dispute within a period of one month from the receipt of the invoice, the recipient shall be deemed to have acknowledged that he is a taxpayer liable to submitting periodic VAT returns. If that condition is not met, the recipient shall be liable in respect of that condition for the payment of the VAT, interests and penalties due.″

Strictly speaking, the contractor should only include this statement on invoices addressed to “small businesses” and “flat-rate farmers”, but in practice it is recommended to always include this text when the VAT is reverse-charged.

The opportunity was also used to extend the reverse charge mechanism to all foreign customers registered for VAT in Belgium. The reverse charge rule will thus apply both to those who have a VAT number with a VAT representative (AVI) and to those who “only” have a so-called direct VAT identification (RBI).

Works outside Belgium

Note that the aforementioned reverse charge rule of RD No. 1, art. 20 only applies if the said works in immovable state take place on the Belgian territory. If the works take place outside Belgium, the VAT rules of the country where the immovable state is located apply. One will then always have to check whether and under what conditions the local VAT can be reverse charged. Possibly it will be necessary to register for VAT in that country.

Foreign contractors

Foreign contractors carrying out works in immovable state in Belgium cannot use the reverse charge scheme of RD no. 1, art. 20. They may be able to use our local reverse charge rule of Art. 51, §2, 5° of the Belgian VAT Code, but (for the time being?) there are no changes taking place in reference to that rule. This means that foreign contractors wishing to apply “VAT reverse charge” still have to check whether their Belgian-based customer submits periodic VAT returns, or whether their foreign-based customer has a VAT representative in Belgium.

Should you have further questions about the reverse charge rules in Belgium, feel free to contact our VAT specialists.